On the morning of March 16, hundreds of depositors gathered outside the headquarters of Asia-Pacific Development Bank in central Phnom Penh, some arriving before dawn. The bank had suspended services five days earlier, citing system maintenance. When it partially reopened, customers could transfer only $300 per day. One depositor told Nikkei Asia she had needed four trips over four days to recover $1,000 in household savings. APD Bank holds over $1 billion in deposits. It did not respond to requests for comment.

Cambodia Investment Review reported the rush was not spontaneous. Bank representatives told the outlet that individuals had contacted ultra-high-net-worth Chinese clients, advising them to withdraw funds based on unverified claims that APD’s license was about to be revoked. The bank called the claims false and described them as the work of actors attempting to undermine institutional confidence. APD was 99 percent owned by a single individual and had grown from founding in 2016 to over $1 billion in assets within eight years.

It was the fourth Cambodian financial institution to face a depositor crisis in four months.

In December 2025, Huione Pay, a licensed payment platform that the US Treasury’s FinCEN had severed from the American financial system for laundering at least $4 billion in proceeds from crypto scams and North Korean cyber heists, collapsed after freezing customer withdrawals during a bank run. In January, Prince Bank was placed into liquidation after its founder Chen Zhi was deported to China on US wire fraud and money laundering charges. The Department of Justice simultaneously filed a civil forfeiture for approximately $15 billion in bitcoin, the largest in American history. In February, the National Bank of Cambodia revoked the license of Panda Commercial Bank, citing deteriorating financial health. CamboJA News reported that Panda’s CEO had previously served as Prince Bank’s chief operating officer and that the bank’s board included a director also listed at Huione Pay.

The personnel chain connecting these institutions raises questions about the scope of what the NBC had under supervision. Huione Pay had been licensed by the NBC before FinCEN documented its role in laundering billions. Prince Bank had operated for years before the DOJ catalogued its parent company’s alleged scam empire. Panda Bank received its commercial license in 2019. The enforcement came from Washington and Beijing. The institutions had been in Phnom Penh all along.

But the scam-sector contagion, as consequential as it is for depositor confidence, is only one of multiple pressures now hitting Cambodia’s banks simultaneously. The IMF, in its November 2025 Article IV consultation, described the country’s risks as “tilted to the downside, driven by financial sector vulnerabilities associated with the array of shocks.” The individual shocks have each been reported. The compound architecture connecting them has not.

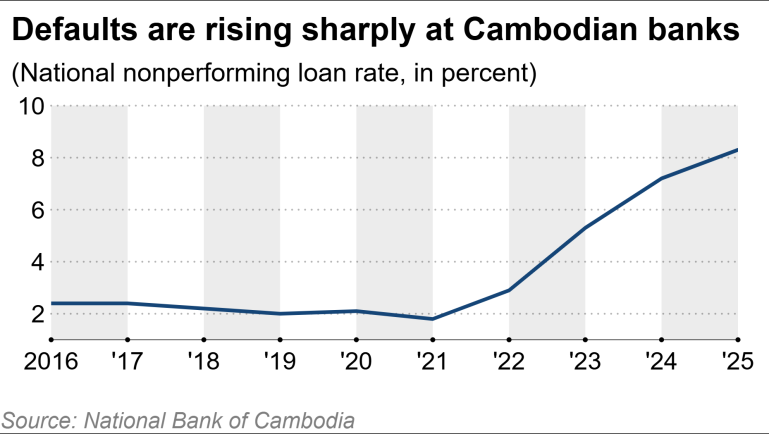

The NBC’s annual report, released in January 2026, put the system-wide non-performing loan ratio at 8.9 percent, up from 7.4 percent in 2024 and roughly 2 percent in 2020. A fourfold increase in five years. At individual institutions the numbers are sharper. NBC data reported by Nikkei Asia showed Phillip Bank at 17.2 percent nonperforming. Hattha Bank, a subsidiary of Thailand’s Krungsri within the Mitsubishi UFJ Financial Group, reported 35.6 percent, driven by microfinance portfolio stress and the broader credit cycle. Hattha’s Thai parentage adds a separate complication: what a foreign parent bank does with a subsidiary carrying that level of impairment, during a period when the parent country and the host country are in a border conflict, is an unanswered question with implications for the broader sector.

How much of the NPL trajectory reflects genuine deterioration and how much is delayed recognition is itself uncertain. The NBC re-launched regulatory forbearance in 2024, allowing banks to restructure troubled loans twice without additional provisioning. AMRO warned the measure “can delay the resolution of the underlying NPL issue” and “poses a moral hazard.” The IMF’s executive board supported phasing it out by the end of 2025 “to enable timely recognition of distressed assets.” Whether the NBC followed through has not been publicly confirmed. If forbearance ended, the 8.9 percent may partly reflect years of suppressed reality finally surfacing. If it continued, the actual impairment rate is higher than what the number shows.

The credit expansion that created the exposure happened fast. Cambodia’s credit-to-GDP ratio rose from 24 percent in 2010 to 135 percent in 2023. The country carries the world’s highest microcredit debt per capita, with approximately 3.1 million microloans worth over $18 billion outstanding across 3.8 million households. Research funded by the Cambodia Microfinance Association found 15 percent of borrowers paying more than 70 percent of monthly income toward debt service.

Much of this lending is collateralized against land whose value has been falling. Prime residential and office property prices in Phnom Penh dropped 34 to 36 percent between mid-2020 and mid-2024, according to Knight Frank. Real estate-related loans account for nearly one-third of total bank lending. The collateral base is eroding under loans that were issued on the assumption it would appreciate. This is not a banking crisis caused by external shocks alone. It is an external shock arriving on top of a structural domestic vulnerability that has been building for over a decade.

The external shocks, though, keep arriving.

The border conflict with Thailand cost Cambodia $700 million in remittances in a single year, according to NBC data. Thailand-sourced remittances fell 27 percent. Roughly 0.9 million workers returned, many carrying microfinance obligations they could no longer service at domestic wages. The NBC implemented emergency fee waivers, payment deferrals, and licence-fee exemptions across five border provinces at a scope that exceeded any comparable NBC intervention in its recent institutional record.

US tariffs compounded the pressure from a different direction. The 49 percent rate announced in April 2025, the highest in Southeast Asia, was eventually negotiated to 19 percent under an agreement requiring Cambodia to eliminate tariffs on all American exports. But the garment sector, which accounts for 45 percent of Cambodia’s export revenue and employs over 900,000 workers, absorbed months of order pauses and factory uncertainty before the settlement. Those workers are also microfinance borrowers. And the agreement is not permanent: President Trump has confirmed the July 9, 2026 deadline for potential reimposition stands. A return to higher tariff rates would hit an already stressed borrower base through a garment sector that employs the same population carrying the microfinance debt.

Then, in March 2026, the global energy crisis from the Iran war and the closure of the Strait of Hormuz reached a country that imports every barrel of oil it consumes and has no domestic refining capacity. Over 2,000 fuel stations were initially affected, with more than 400 still closed as of mid-March. Gasoline prices jumped from 3,850 to 4,400 riel per liter within days. The Mines and Energy Minister disclosed strategic reserves of 21 days. The government cut fuel import taxes from 10 to 4 percent. Cambodia had also narrowed its own supply base: during the border conflict, it imposed a ban on Thai imports including fuel as an economic countermeasure, while the closure of all 18 official land crossings independently disrupted overland supply routes. A sovereign decision and a conflict consequence, compounding simultaneously, before the global crisis tightened supply further.

Ky Sereyvath, an economist at the Royal Academy of Cambodia, warned in Khmer Times that sustained fuel price increases could trigger a “credit crisis” that “could destabilise the entire banking system.” He was describing the mechanism by which the energy shock connects to everything already in motion: fuel costs compress household budgets, compressed budgets produce loan defaults, defaults accelerate NPL growth in a system where three banks and a major payment platform have already failed or frozen withdrawals in four months.

On conventional indicators, none of this constitutes systemic crisis. The capital adequacy ratio sits at 22 percent, seven points above the regulatory floor. Deposits grew 14.7 percent in 2025. AMRO’s Jinho Choi told Nikkei Asia there was “no systemic risk to the banking sector, given adequate capital buffers.” Jayant Menon of the ISEAS-Yusof Ishak Institute called the bank crises “a few bad apples.” The NBC told Nikkei the APD situation was “not reflective of the banking sector’s broader stability.”

These assessments describe what the buffers can absorb. They do not describe what happens when multiple shocks test those buffers at the same time, through a safety net with specific structural gaps that have been documented for years.

Cambodia is the only country in ASEAN, apart from Myanmar, that lacks a deposit insurance scheme. The gap has been documented since at least 2015. AMRO published a detailed case for establishing one in 2024. The IMF’s executive board encouraged its creation last November. The NBC has signed a cooperation agreement with Korea’s KAMCO and established an internal unit to develop the architecture. None of it was in place when depositors at Prince, Panda, and APD needed it.

The economy’s heavy dollarization creates a second gap. Most deposits are in US dollars. AMRO has stated directly that the NBC “cannot fully perform its role as the lender of last resort by injecting USD liquidity into a bank when there is a bank run.” The NBC updated its emergency lending framework on March 21, five days after the APD rush. Menon questioned whether riel liquidity would meet dollar obligations.

The NBC’s broader institutional response has been both substantive and fast. It liquidated the scam-linked banks and appointed administrators to protect depositors. It issued regulations in February creating asset management institutions to acquire nonperforming loans, modeled on mechanisms that Indonesia, Malaysia, Korea, and Thailand deployed after the 1997 financial crisis. Minimum registered capital was set at $50 million. Governor Chea Serey addressed the public directly on Facebook, explaining bank run mechanics without naming APD, then released a second video for Prince and Panda depositors. The government deported Chen Zhi, revoked his citizenship, and demonstrated enforcement capacity against networks that had operated under domestic supervision. The AMI framework targets NPL resolution. The updated lender-of-last-resort protocol targets liquidity provision. The enforcement actions target financial integrity. The relief directives target border-province borrower stress.

Each response targets one vector. No response, and no combination of them, addresses the compound interaction of all vectors arriving within fifteen months in a system without deposit insurance, with a dollarization constraint on its central bank, with forbearance potentially masking the true depth of impairment, and with a credit-to-GDP ratio that quintupled in thirteen years.

A depositor at Panda Bank told Nikkei Asia his trust in the banking system was “nearly 0 percent.” He was not responding to one bank’s failure. He was carrying the weight of the compound in a system where nothing guaranteed his savings. He could not name it. The scam-sector stories had run as scam stories. The NPL data ran as banking data. The tariff coverage ran as trade policy. The energy crisis ran as geopolitics. The border conflict ran as security. Each piece visible. The architecture connecting them, not.

Cambodia’s banking system has not collapsed. The capital buffers are real. The deposit growth is real. The institutional response is real. The compound is also real. It is producing effects no single-vector analysis can account for: four financial institution crises in four months, a central bank governor explaining bank runs on Facebook, and the crisis management architecture of a $30 billion economy being assembled while the shocks it was designed to absorb are already underway.