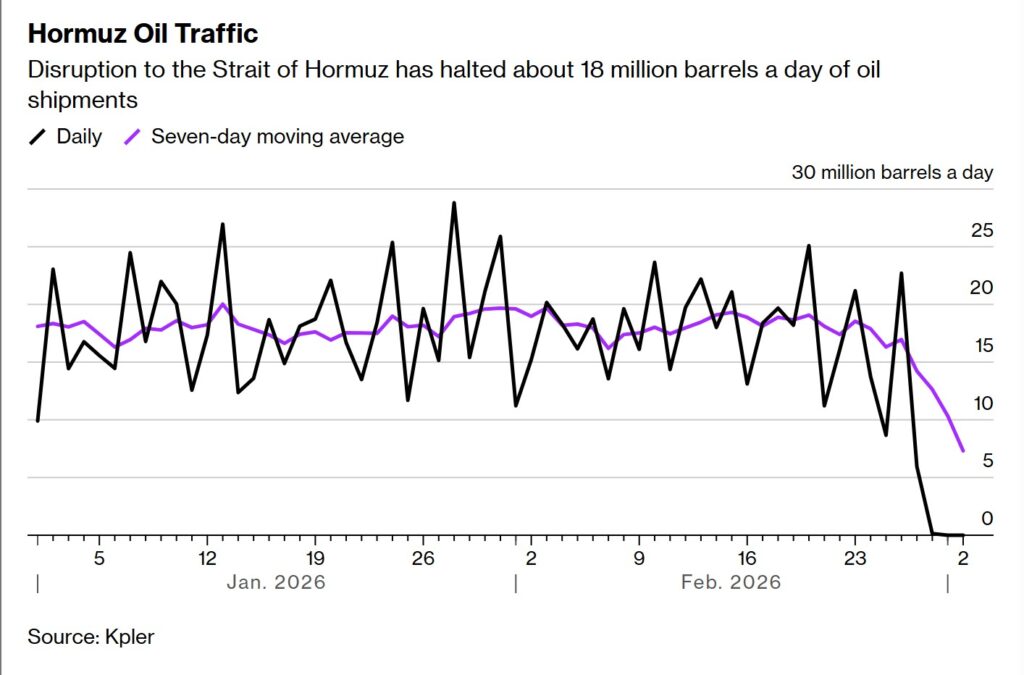

The escalation of the US–Iran conflict is now expressing as an energy-security event, not only a military one. Bloomberg reported that tanker traffic through the Strait of Hormuz fell 94% on March 1, citing the Joint Maritime Information Center, a level that if sustained would effectively choke one of the world’s most important seaborne energy corridors. Reuters separately reported that Iranian strikes disrupted multiple energy nodes across the Gulf, including Qatar’s Ras Laffan LNG complex described by Reuters as responsible for about 20% of global LNG supply and Saudi Arabia’s Ras Tanura refinery.

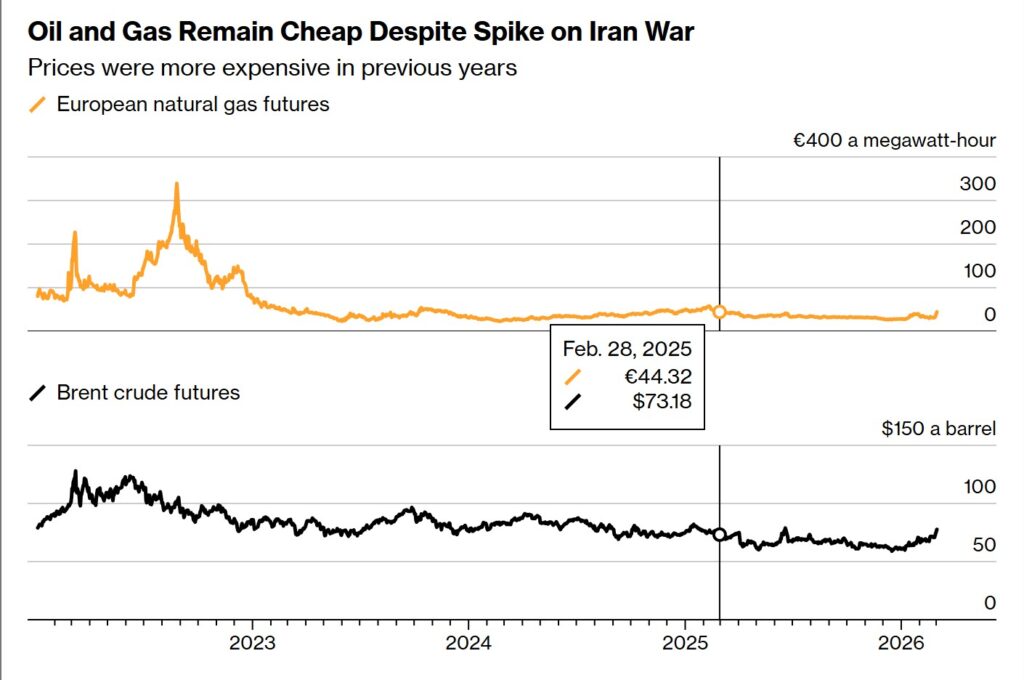

Market pricing has moved sharply, but not yet in proportion to the physical shock described in the reporting. Bloomberg said Brent crude jumped as much as 14% when markets opened after the weekend’s escalation, before trading around the high-$70s per barrel, while European gas surged sharply on the prospect of a large LNG supply interruption. Reuters likewise described oil and gas prices rising on shipping disruption and infrastructure hits, while emphasizing that the duration of disruption especially in LNG will determine whether volatility becomes a broader inflation and supply-chain problem.

The divergence between oil’s price response and LNG’s fragility is structural. Oil is globally fungible and supported by strategic stocks, diversified supply chains, and multiple routing and substitution options; LNG is constrained by tight liquefaction capacity and thinner storage buffers, meaning a large outage can migrate quickly from price moves into allocation and demand destruction. Reuters’ description of Ras Laffan’s scale and its concentration of infrastructure frames the immediate risk: when a single complex supplies a large share of global LNG, the replacement problem is physical before it is financial.

Europe sits on the front line of that constraint because LNG is the marginal balancing molecule for many European systems, and because gas price spikes transmit quickly into industrial costs, household bills, and fiscal pressure. While the European Commission has signaled coordination and monitoring rather than declaring an immediate emergency, the political breakpoint historically comes when governments are forced into large-scale support for utilities and consumers, or into explicit rationing mechanisms. In the current episode, Reuters’ reporting underscores that the shock is not only the commodity price but the tightening of logistics and risk shipping, insurance, and availability which can convert a “high price” market into a “no cargo” market.

Northeast Asia operates under a different constraint set: reliability and grid stability dominate the short-term response, then domestic price politics and utility solvency define the medium-term ceiling. Japan and South Korea are structurally exposed because they lack Europe-scale underground storage and rely heavily on LNG for power; they mitigate through stockholding, emergency procurement, demand restraint, and fuel-switching ladders documented by the IEA in its crisis-response and country security frameworks. In a sustained disruption, that architecture implies a two-phase behavior: pay up and secure prompt cargoes while blackout risk is salient, then shift toward administrative demand suppression when the marginal price becomes politically destabilizing.

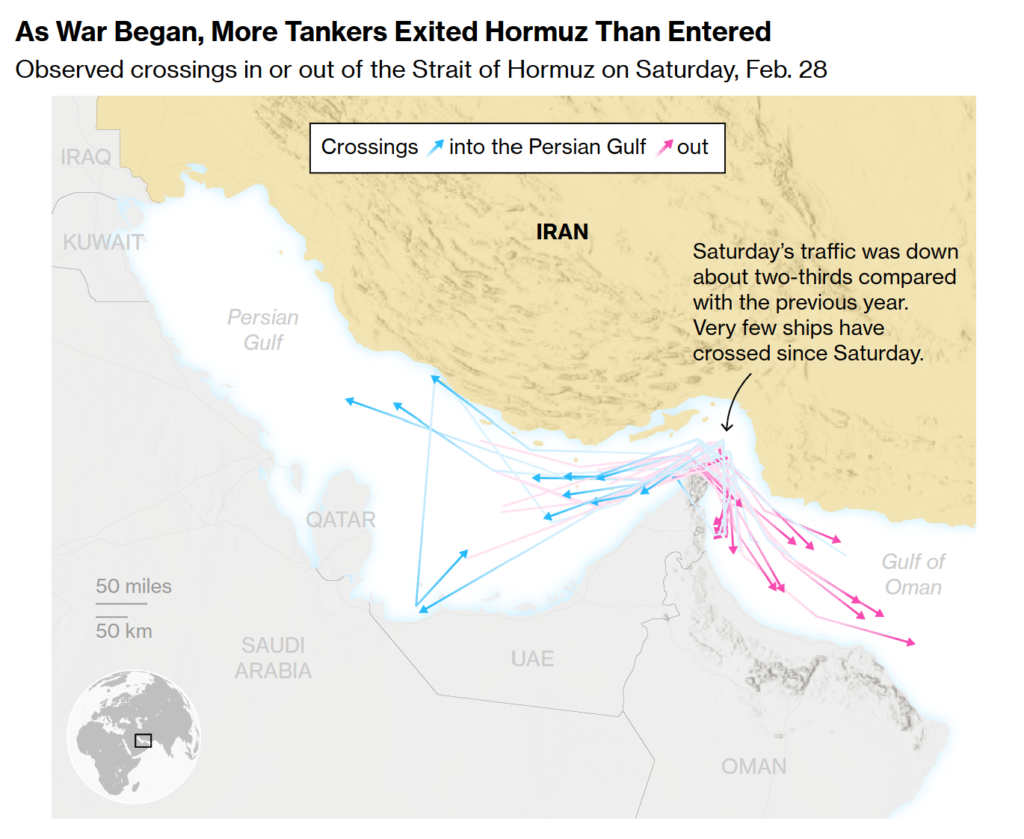

Note: The map shows only ships passing through the straits; other ship traffic is not captured. Ship paths are straight-line interpolations between positions transmitted by ships and may not reflect actual traveled routes. Tanker types includes oil, LNG and LPG.

This sets up an intra-alliance tension around LNG redistribution, because the United States now a major LNG exporter can allow market clearing through price (supporting exporters but forcing allies into a bidding contest), or intervene through policy levers that effectively allocate volumes (protecting allies but potentially lifting domestic prices), or restrict exports (shielding domestic consumers at alliance cost). The “shale insulation” argument is also incomplete on its own terms: Reuters reported US gasoline prices rising to levels not seen since late 2025, underscoring that even high domestic production does not fully decouple consumer prices from global benchmarks and geopolitical risk premia.

Secondary actors have obvious arbitrage incentives if disruption persists. Russia benefits from higher energy prices and can seek political leverage by offering marginal supply pathways at moments of European stress; China is comparatively more insulated due to diversified pipeline inflows and larger buffers, allowing it to posture as mediator or opportunistic buyer in dislocated markets. The strategic point is that a prolonged Hormuz-linked disruption is not only an energy-price problem; it is an alignment stress-test in which allies face asymmetric exposure and therefore asymmetric urgency. Reuters’ shipping-rate reporting captures the practical mechanism: when war-risk premia surge and carriers avoid the corridor, “duration” becomes the dominant variable markets can tolerate spikes, but systems break on sustained constraints.

The decisive question, then, is time. If Hormuz transits normalize and Ras Laffan resumes in days, the market can reprice quickly and much of the premium can compress. If disruption extends into weeks, the stress migrates from trading books to treasury decisions and emergency policy subsidies, rationing, fuel-switching, and diplomatic pressure because energy stops behaving like a market fluctuation and starts behaving like a fiscal event with alliance consequences. Bloomberg’s central point that traders appear to be betting on a short conflict despite unusually large disruptions frames the mismatch: the market may be underpricing the political and physical costs of duration.